Independent Benefit Advisors offer short term individual health care plans, employee group health insurance and medicare services as well as dental coverage …

The best people want to work for the best employers. Now, more than ever, organizations must consistently offer beneficial incentives that keep employees happy and engaged — which contributes to greater customer loyalty and business longevity.

By Lindsay Mather, Vice President of Human Resources

What truly makes a business successful?

Arguments can be made for having a superior and desirable product or service; an influential and recognizable brand; or a loyal and satisfied customer base.

While these are all important, I believe employees hold the key that unlocks the door to business longevity.

Think about it — your employees interact with clients, prospects and vendors to build the relationships, grow your brand and make the sales your business relies on. And it’s no secret that employees who are happy and engaged at work tend to deliver better customer service.

As businesses are constantly vying to attract and retain top talent, you can’t just hope to hire the best. Your organization must work hard to consistently provide compelling incentives so the best want to work for you.

Competitive wages and benefits are still important to employees. But to really standout in today’s hiring market, employers must also prioritize creative solutions that foster the strong company cultures employees are increasingly expecting, including:

Respect, autonomy and empowerment

Professional and personal wellbeing

Connection and enjoyment

I am proud to say that Rogers Insurance’s efforts in these areas has resulted in us being recognized yet again as one of Alberta’s Top Employers (this is our 14th such recognition).

Respect, Autonomy & Empowerment

To be truly engaged and satisfied at work, employees must feel respected.

Respect in the workplace isn’t limited to kindness, fairness and inclusion; it’s also about trusting and empowering your employees to truly take ownership of their work. This requires providing a certain level of autonomy, which is why Rogers Insurance has purposefully created a fairly flat structure and non-bureaucratic environment.

For example, our bereavement leave policy is purposefully open-ended. We recognize that everyone grieves differently and that we all have a variety of important people in our lives; no longer are just relatives considered family. Therefore, we have not defined a set number of leave days in the event of the passing of someone important. Instead, we approve bereavement leave on a case-by-case basis that is handled with the utmost respect for an employee’s personal needs to grieve and honour their loved one.

Another example is that our dress code policy — which we call Dress for Your Day — permits staff to wear more relaxed attire (i.e., jeans) any day of the week, as appropriate, so long as it remains professional.

We also offer our employees a share ownership plan through which employee owners share in the success and growth of our company. These employee ownership models are becoming increasingly rare and we are proud to offer this unique incentive to our staff.

Professional & Personal Wellbeing

Investing in employees’ professional success is something many employers can claim (including Rogers Insurance, where some of our initiatives include in-house training and financial support for courses and licensing requirements).

But employees are also looking for their employers to contribute to their personal wellbeing. This can include:

Wellness initiatives: For example, in our Calgary office we have a Peloton bike, cruiser bikes and e-scooters onsite that staff can use throughout the day; a private and comfortable Spa Room where staff can take a break; and an employee-run Wellness Committee, which arranges a variety of wellness and mental health activities for our people to engage in.

Wellness breaks: For example, our staff receive flex days in addition to their vacation allotment. These flex days can be used at their discretion, such as taking a mental health break.

One of the most unique ways that Rogers Insurance invests in its people, however, is our Dream Program.

Dreams inspire and give people purpose and hope, which is exactly what we want for our staff. Through our Dream Program, we randomly award four employees each year with up to $10,000 to fulfill a once-in-a-lifetime experience of their choosing.

This program is distinct within the insurance industry and demonstrates that we truly care for the professional and personal wellbeing of our people.

Connection & Enjoyment

We spend, on average, a third of our waking hours working.

This significant investment of time underscores, for me, the importance of providing an enjoyable workplace culture that fosters connectivity. People thrive when they are happy and connected — this is true personally and professionally. That’s why one of Rogers Insurance’s core value focuses on fun.

Our employee-run Fun Squad works diligently to provide engaging activities year-round. This includes everything from our highly anticipated annual Halloween costume contest and Broker Ball slow pitch game to candy grams, virtual events and much more. This year, the Fun Squad is even planning a private screening of a newly released movie for staff to enjoy (the selected movie will be the one with the most staff votes).

These initiatives do much more than just inject a healthy dose of fun into the workplace; they also encourage our people to interact and form relationships with all of their colleagues, not just those on their own team.

Simply put, the best people want to work for the best employers. Gone are the days (and rightly so!) where employers can expect great results from their staff while offering very little in return. Organizations must continue to evolve and create incentives in order to keep employees engaged and happy — which in turn contributes to greater customer satisfaction and business longevity.

Lindsay Mather is the Vice President of Human Resources at Rogers Insurance. She is passionate about creating HR initiatives that contribute to a positive, productive and fun culture that benefits the organizations and encourages employees to be successful.

http://www.MurrayGRP.com/ – #97 – Hit-and-run accidents happen and they are terrible. You go into a shopping mall and come out to find that someone hit your …

Is Universal Life Insurance a Good Product? Get a FREE customized plan for your money. It only takes 3 minutes! http://bit.ly/2YTMuQM Visit the Dave Ramsey …

Where you live could mean the difference between life and death. Subscribe to our channel! http://goo.gl/0bsAjO Vox.com is a news website that helps you cut …

Certain expenses in life are out of your control. As nice as it’d be, we cannot adjust gas prices to our liking. However, when it comes to auto insurance, most insurers offer dozens of discounts that can help you save significantly. In fact, chances are you may be eligible for some auto insurance discounts you didn’t even know existed.

Most providers offer discounts that fall into the following categories: driver safety, driver status, policy, vehicle, and usage based. To maximize your savings, we put together a list of common discounts many insurers offer. Insurance policies and availability vary greatly depending on where you live, so always speak to an insurance specialist to learn about the discounts available to you.

Driver Safety Based Discounts

Driver safety discounts reward those with safe driving habits. If you’ve never been in an accident, or if you have taken a defensive driving course, these auto insurance discounts can help you reduce your monthly premium.

Good driver discount: If you’ve been licensed for at least three years, have one or fewer points on your record, and haven’t been in an injury accident, you may be eligible for a good driver discount.

Defensive driving course discount: Defensive driving courses can help prevent accidents, which is why some insurers offer policyholders reduced rates for completing them. These classes can help drivers better assess road, weather, and traffic conditions to avoid accidents. Depending on the state, this discount may only be available to senior drivers.

Claim-free discount: If you’ve gone more than five years since your last claim, you may be eligible for a claim-free discount.

Driver Status Based Discounts

Driver status discounts are also based on the driver, but not their specific driving habits. Depending on your age and where you work, you may be eligible for discounts just for being who you are.

Good student discount: It’s no secret that younger drivers are some of the most expensive people to insure. However, let’s suppose you’re a full-time student, under 23, and maintain a B average. In that case, you may qualify for a good student discount. Keep in mind, most providers typically require you to provide proof of your academic standing to apply this discount.

Mature driver discount: Another year older means another year wiser, but it can also mean saving on auto insurance. Typically, drivers with more driving experience are less risky to insure. Depending on your provider, you may qualify for a senior discount if you’re over the age of 55.

Association discount: Some providers offer discounts for those involved with associations like AAA, Costco, Sam’s Club, and more.

Profession/Education discount: Certain professions as less riskier than others. You may receive a discount because of your profession, membership in a professional organization or level of education.

Away-from-home student discount: As a parent, you can save monthly on your auto insurance if you have a child driver that’s away from their covered vehicle. These discounts tend to apply to child drivers more than 100 miles from home.

Policy Based Discounts

These auto insurance discounts are based on the type of policy you have with your provider. In fact, you can adjust your policy in various ways to take advantage of these specific discounts. While these discounts are often automatically applied, you may need to request them with your insurance specialist.

Multi-policy discount: Multi-policy discounts can help families save significantly. They are also some of the easiest to qualify for if you have multiple drivers under one roof. In addition, bundling your auto insurance with other lines of coverage, such as a homeowner’s policy, can open the door to increased savings.

Electronic billing/autopay discount: If you have a policy through a major company, you may be able to save on your premium if you opt for electronic billing or enroll in autopay. Another possible discount is often available for “Good Payers”, which are policyholders with no late payments or non-sufficient funds charges within a specific timeframe.

Pay in full discount: Insurers often offer discounted annual premiums for those who can pay for their coverage in full. When shopping for insurance, keep an eye out for this discount as it tends to be a separate option on most quote pages.

Vehicle and Usage Based Discounts

Depending on the vehicle you own, and how often you use it, you may be eligible to receive a reduced rate. Some vehicle discounts could require components to be factory-installed, so always double-check with your insurance specialist.

Anti-theft discount: Vehicles that have anti-theft systems installed help to reduce the chance of theft making them less risky to insure. As a result, insurers often reward drivers that take the extra steps to protect their vehicle.

Vehicle Usage Based Discounts: Insurance companies are increasingly adopting rates based on mileage verification (in California) that use devices or apps to track your actual vehicle usage (telematics). Check if your company offers one of these discounts.

Save On Auto Insurance by Comparing Rates

There are plenty of auto insurance discounts available that you can take advantage of to lower your auto insurance rate. A good insurance agent will know what questions to ask to help you find as many as possible. You can always kickstart your savings by comparing insurance quotes. If you’re ready to find the best combination of rates, coverage, and discounts, give our specialists a call at (855) 919-4247.

The information in this article is obtained from various sources and offered for educational purposes only. Furthermore, it should not replace the advice of a qualified professional. The definitions, terms, and coverage in a given policy may be different than those suggested here. No warranty or appropriateness for a specific purpose is expressed or implied.

Certain auto insurance carriers can issue policies with foreign, international, suspended licenses or no license at all, depending on a their underwriting …

A major premise of the Affordable Care Act (ACA) was that Americans who need to buy their own health coverage in the individual market should be able to obtain coverage – regardless of their medical history – and that the monthly premiums should be affordable.

The rules to facilitate those goals have been in place for several years now. And although they have worked quite well for some Americans, there have been others for whom ACA-compliant health coverage was still unaffordable.

But the American Rescue Plan, enacted earlier this year, has boosted the ACA’s subsidies, making truly affordable coverage much more available than it used to be.

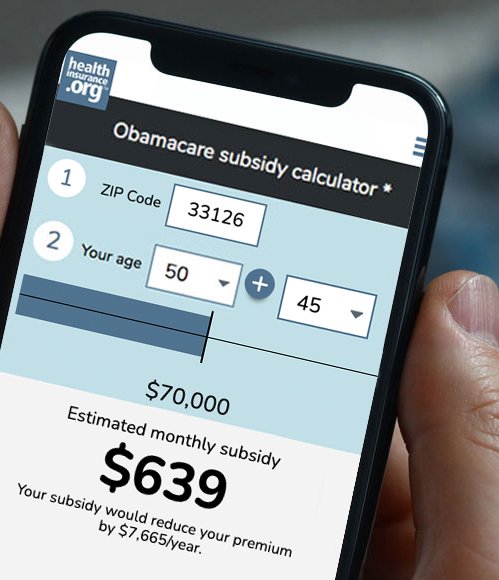

The numbers speak for themselves: Exchange enrollment has likely reached a record high of nearly 13 million people in 2021, after more than 2.5 million people enrolled during the COVID/American Rescue Plan enrollment window, which ended this month in most states.

How much are consumers saving on health insurance premiums?

And the amount that people are paying for their coverage and care is quite a bit lower than it was before the APR’s subsidy enhancements. We can see this across the states that use the federally run exchange (HealthCare.gov), as well as the states that run their own exchanges:

Among the people who enrolled during the recent special enrollment period in the 36 states that use HealthCare.gov, average after-subsidy premiums were 27% lower than the amounts people were paying pre-ARP.

Among HealthCare.gov enrollees who signed up during the special enrollment period or who updated their enrollments to claim the enhanced subsidies, 35% are now paying less than $10/month for their coverage.

Average deductibles for new HealthCare.gov enrollees were 90% lower than pre-ARP deductibles, likely driven in large part by the number of people who were able to enroll in free or low-cost Silver plans with built-in cost-sharing reductions. (This includes people receiving unemployment compensation in 2021, as well as people who aren’t eligible for Medicaid and whose household income is between 100% and 150% of the federal poverty level.)

The state-run exchange in Washington reported that 78% of their enrollees are now receiving premium subsidies, versus 61% before the ARP was implemented. And consumers with income above 400% of the poverty level, who were not eligible for subsidies pre-ARP, are now paying an average of $200 less in premiums each month. Washington’s exchange also noted that 15% of their enrollees are now paying $1/month or less for their coverage, versus only 5% whose premiums were that low pre-ARP.

The state-run exchange in California reported that consumers with household incomes between 400% and 600% of the poverty level are saving an average of almost $800/month on their premiums. (That’s an individual with income up to about $76,000, or a household of four with an income up to about $157,000.)

The state-run exchange in Nevada reported that people who enrolled or updated their account since the ARP was implemented are paying an average of $154/month in after-subsidy premiums, whereas the after after-subsidy premium at the end of last winter’s open enrollment period (pre-ARP) was $232/month.

Maryland’s state-run exchange reported a 12% increase in the number of enrollees receiving subsidies; more than 80% of Maryland’s current exchange enrollees are subsidy-eligible.

These examples highlight the improved affordability that the ARP has brought to the health insurance marketplaces. People who were already eligible for subsidies are now eligible for larger subsidies. And many of the people who were previously ineligible for subsidies — but potentially facing very unaffordable health insurance premiums — are benefiting from the ARP’s elimination of the income cap for subsidy eligibility.

How long will the ARP’s subsidy boost last?

Although the ARP’s subsidies for people receiving unemployment compensation in 2021 are only available until the end of this year, the rest of the ARP’s premium subsidy enhancements will continue to be available throughout 2022 — and perhaps longer, if Congress extends them.

Use our updated subsidy calculator to estimate how much you can save on your 2021 health insurance premiums.

This means that the affordability gains we’ve seen this year will be available during the upcoming open enrollment period, when people are comparing their plan options for 2022.

Robust ACA-compliant coverage will continue to be a more realistic option for more people, reducing the need for alternative coverage options such as short-term plans, fixed indemnity plans, and health care sharing ministry plans.

Even catastrophic plans – which are ACA-compliant but not compatible with premium subsidies – are likely to see reduced enrollment over the next year, since more people are eligible for enhanced subsidies that make metal-level plans more affordable.

Can everyone find affordable health insurance now?

Unfortunately, not yet. There are still affordability challenges facing some Americans who need to obtain their own health coverage. That includes more than two million people caught in the “coverage gap” in 11 states that have refused to expand eligibility for Medicaid, as well as about 5 million people affected by the ACA’s “family glitch.”

There are strategies for avoiding the coverage gap if you’re in a state that hasn’t expanded Medicaid, and Congressional lawmakers are also considering the possibility of a federally-run health program to cover people in the coverage gap.

Families affected by the family glitch have access to an employer-sponsored plan that’s affordable for the employee but not for the whole family – and yet the family is also ineligible for subsidies in the marketplace/exchange. (It’s possible that the Biden administration could tackle this issue administratively in future rulemaking.)

Have ARP’s subsidy boosts been successful?

With the exception of those two obstacles, the ARP has succeeded in making affordable health coverage a more realistic option for most Americans who need to obtain their own health coverage. We can see success in the record-high exchange enrollment, the increased percentage of enrollees who are subsidy-eligible, and the reduction in after-subsidy premiums that people are paying.

If you’re currently uninsured or covered by a non-ACA-compliant plan (including a grandfathered or grandmothered plan), it’s in your best interest to take a moment to see what your options are in the ACA-compliant market. Open enrollment for 2022 coverage starts in just two months, but you may also find that you can still enroll in a plan for the rest of 2021 if you live in a state where a COVID/American Rescue Plan enrollment window is ongoing, or if you’ve experienced a qualifying event recently (examples include loss of employer-sponsored insurance, marriage, or the birth or adoption of a child).

Even if you shopped just last winter, during open enrollment for 2021 plans, you might be surprised at the difference between the premiums you would have paid then and now. The ARP wasn’t yet in effect during the last open enrollment period, so if you weren’t eligible for a subsidy last time you looked, or if the plans still seemed too expensive even with a subsidy, you’ll want to check again this fall.

The subsidies for 2022 will continue to be larger and more widely available than they’ve been in the past, and you owe it to yourself to see what’s available in your area.

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written dozens of opinions and educational pieces about the Affordable Care Act for healthinsurance.org. Her state health exchange updates are regularly cited by media who cover health reform and by other health insurance experts.

Have you heard the “buy term and invest the difference” argument? This philosophy is widely held but more specifically is the advice of Dave Ramsey and Suze …

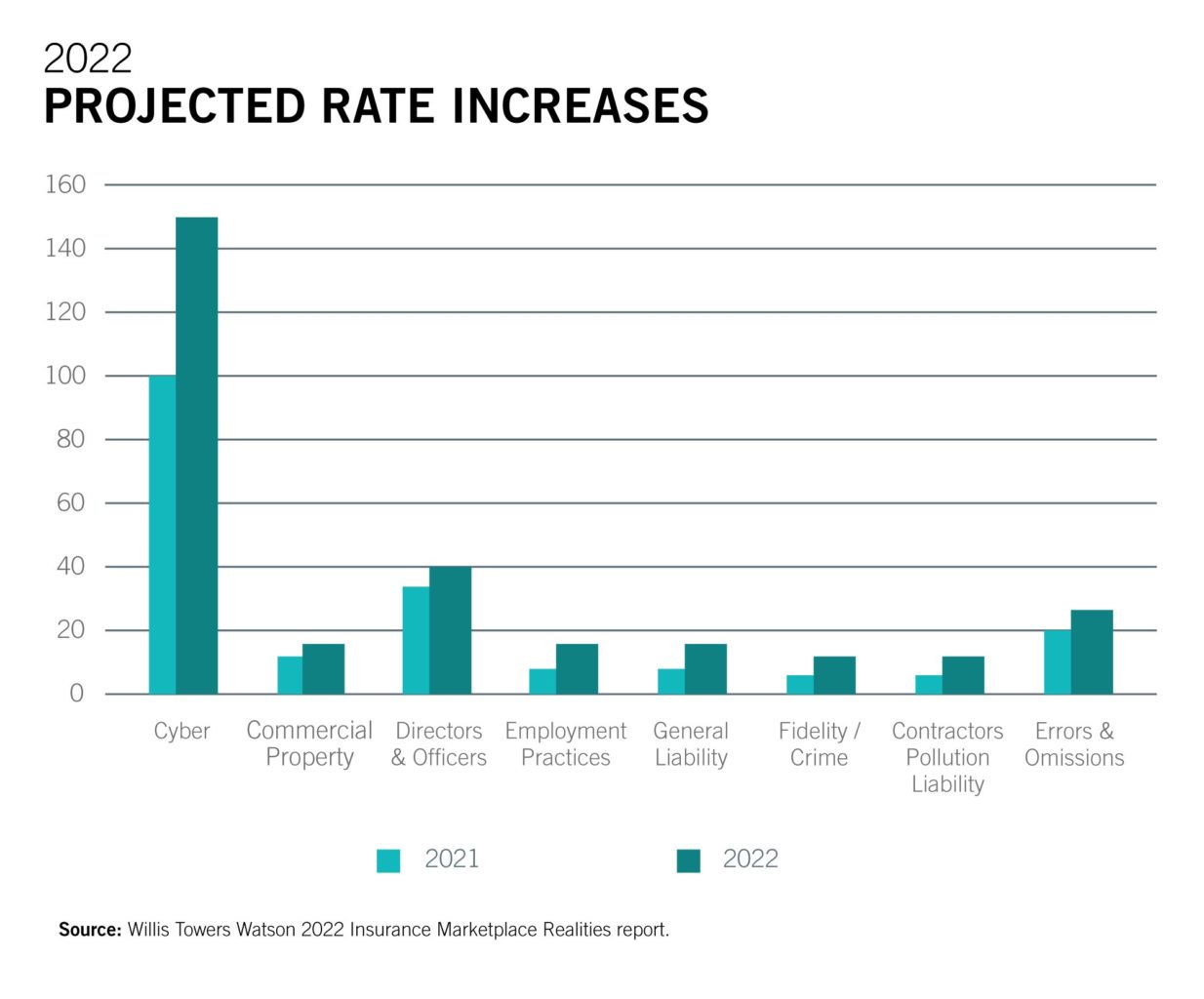

The hard market challenges of the past few years will continue into 2022. But there is good news — things are starting to stabilize as insurers ease rate hikes for some coverages and industries and increase capacity to underwrite certain risks.

Businesses should still anticipate rate increases in 2022, depending on their sector. Some estimates state the average increase will be single digit; however, insurers are increasingly focusing on specific lines of liability coverage and double-digit hikes are expected for certain lines that have experienced high losses — cyber liability in particular.

“While the industry is performing better, insurers will increasingly be more selective in who they choose to insure,” says Lee Rogers, President, Rogers Insurance Group of Companies. “Underwriting scrutiny and a better understanding of risk management and loss control will continue.”

What’s Driving Rate Increases?

Cybercriminals are consistently launching more aggressive attacks on companies of all sizes, resulting in steeper and more frequent claims.

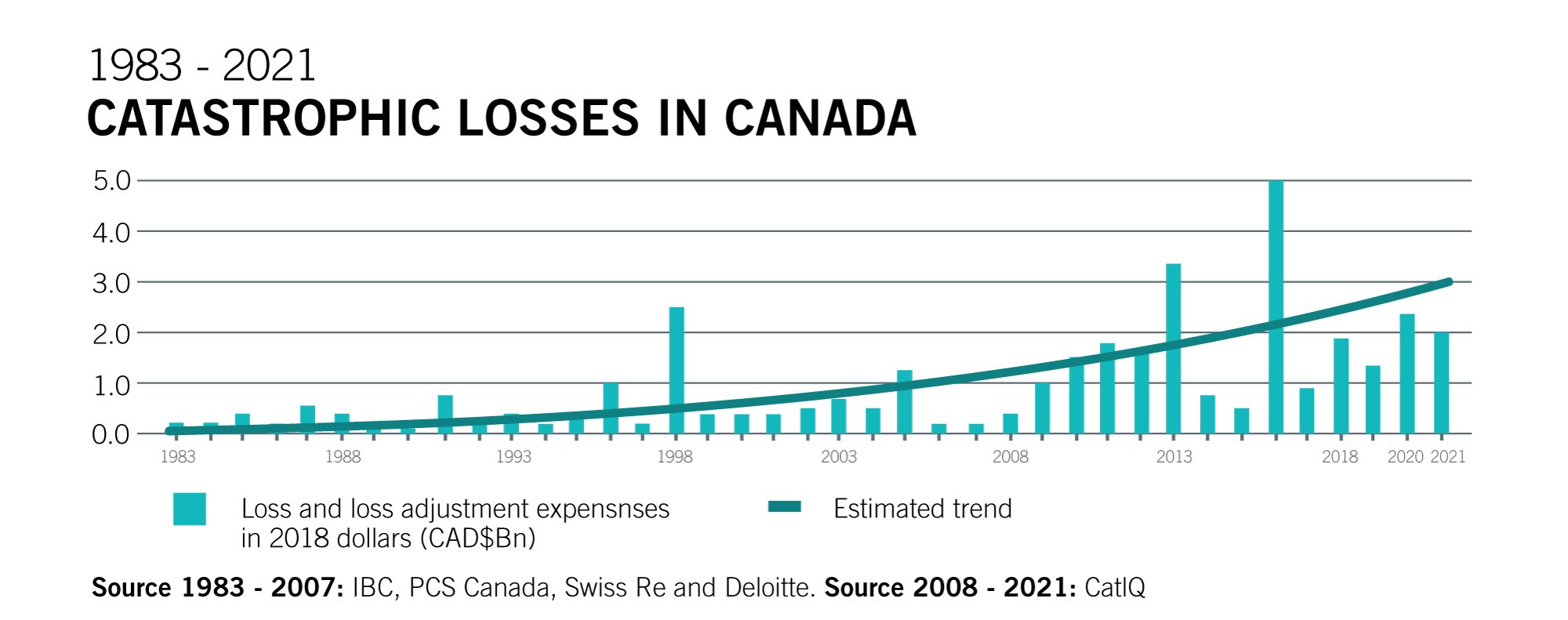

Climate change is causing more severe and frequent catastrophic natural events, leading to higher losses.

Repair and replacement costs have spiked due to several factors, including increased costs for raw materials; material and labour shortages; global supply chain issues; and inflation.

Historically low interest rates are impacting insurers’ overall profitability.

Catastrophic and attritional losses are increasing in severity and occurrence, which continues to strain the insurance industry.

Trends That Will Impact Your Insurance in 2022

COVID-19 has affected and, in many cases, amplified social, economic and financial challenges, which in turn impacts insurance (i.e., higher rates, evolving risk mitigation tactics that underwriters require). Here are four trends we anticipate will impact your insurance in 2022.

Cyber Threats

Cyber claims are drastically on the rise with hackers consistently launching more severe and sophisticated attacks. Couple this with the rapid transition to remote work in 2020, and businesses of all sizes are more susceptible to cyberattacks.

Furthermore, political tensions have caused some insurers to add exclusions related to state sponsored attacks to their cyber products. For example, Lloyd’s of London announced in November 2021 it will no longer cover losses that result from ‘cyber war,’ which is when one country launches a cyberattack against another.

Due to the high-level of cyber risk, underwriters are scrupulously examining an organization’s cyber hygiene practices.

What You Can Do:

Strengthen your perimeter security. Close and replace all unnecessary remote desktop protocols with a secure VPN that is protected by multi-factor authentication.

Strengthen your email security. Use multi-factor authentication and regularly educate your staff on how to spot and respond to attempted breaches (i.e., phishing attacks).

Strengthen your data security. Regularly back up your company data on at least two different kinds of media — including one stored safely offsite. Also regularly test your backups to ensure your data is accessible and readable.

Speak with your broker about your current cyber coverage and also about additional mitigation efforts that can help protect you from a cyberattack.

The average total cost to recover from a ransomware attack was $1.85 million in 2021—more than double from the year before.

(Source: The State of Ransomware 2021)

Environmental, Social & Governance Policies

Insurers are increasingly scrutinizing companies’ environmental, social and governance (ESG) policies and performance. Issues such as pollution, diversity and inclusion, and corporate conduct have been receiving greater public attention, resulting in more litigation.

This has resulted in underwriters examining ESG to assess a company’s liability risk and potential exposures.

What You Can Do:

Prioritize your company’s ESG policy, including enacting procedures and protocols for monitoring, tracking and reporting on progress.

According to the Allianz Global Corporate & Specialty report released in October 2021, five ESG risks to be aware of are:

Climate change and pollution: What is your company doing to reduce its carbon footprint?

Board diversity: Does your board have diverse representation?

Greenwashing: Is your company setting realistic environmental goals? Exaggerating your performance will backfire.

CEO performance: Would your company consider measuring your leader’s performance to successful ESG outcomes?

Cybersecurity: What is your company doing to reduce its risk of a cyberattack?

78% of insurers believe COVID-19 accelerated their focus on ESG.

(Source: BlackRock)

Global Supply Chain Issues

Challenges exasperated by the pandemic (i.e., product and staffing shortages) and climate change have exposed just how vulnerable the global supply chain is.

The strain this has put on businesses has highlighted the need to prioritize business continuity planning and diversification of materials and suppliers — things that insurers are looking for.

What You Can Do:

Conduct a thorough risk assessment to identify ongoing and emerging local, regional, national and global disruptions that could affect your business operations.

Review, enhance and test your business continuity plan. Outline how your business will respond to a disruption, including plans for staffing, inventory and storage, supplier backups, communication and more.

Determine how you can diversify your organization’s supply chain — your suppliers, the products and materials you use, and how these items travel to you.

70% of Canadian supply chain organizations have experienced supply chain disruptions as a direct result of COVID-19 implications.

(Source: Supply Chain Canada)

COVID-19

The focus on COVID-19 has shifted from how to conduct day-to-day business to how to keep employees safe, manage vaccine compliance and avoid lawsuits.

Litigation against employers as it relates to virus, however, is starting to increase in Canada. Cases are diverse, ranging from failure to provide a safe and healthy workplace, to wrongful termination, discrimination, vaccination policy disputes and more.

As a result, insurers are re-examining the level of risk they’re willing to assume, which is impacting the cost and ability to secure certain coverages — employment practices liability and directors and officers liability in particular.

What You Can Do:

Follow all government and health authority requirements in each of the jurisdictions where your organization operates. Clearly communicate all measures that staff need to follow and document your compliance.

Consult with a qualified lawyer on any return-to-work protocols or vaccine mandates; they can identify and advise on how to remedy any potential gaps that may leave you vulnerable to a liability claim.

Implement reasonable measures to maintain the privacy of your employees, including any coronavirus-specific details you may collect (i.e., positive tests, vaccination records).

Lawyers anticipate a spike in employment practices lawsuits related to COVID-19, ranging from privacy breaches to failure to comply to public health guidelines.

(Source: Levitt Sheikh Employment Labour Law)

These trends underscore how crucial it is to prioritize extensive risk assessment and management. Contact us to discuss ways your business can mitigate risk.

Prof. Jochen Klucken (Vice Head of the Department of Molecular Neurology, University Hospital Erlangen) speaks about “Getting off the Ground: Digital Health …